In 1865, the English economist William Stanley Jevons published The Coal Question. Britain was burning through its reserves at an unprecedented rate, and engineers had just made the steam engine far more efficient. The popular assumption was simple. A more efficient engine would burn less coal. Jevons argued the opposite. Cheaper, more productive use of coal would expand the universe of things coal could power, and demand would rise rather than fall. He was right. British coal consumption climbed for decades after.

That observation, now known as the Jevons Paradox, has become one of the most quoted economic arguments in the AI debate of the mid 2020s. Microsoft chief executive Satya Nadella has cited it. Apollo Global Management's chief economist Torsten Slok has built what he calls a "Jevons employment effect" thesis around it (Fortune, 2026). The question those leaders are wrestling with is not whether AI will make individual workers more productive. That part is settled. The open question is whether the productivity gain will hollow out the workforce or, in line with Jevons, expand it in new and unexpected directions.

For people leaders, the answer matters more than for almost anyone else. The recent record is messy. Tech and fintech firms have run a visible cycle of "AI attributed" layoffs followed, sometimes within months, by quiet rehiring. Klarna, IBM, and Duolingo have all become case studies in 2025 for the limits of efficiency thinking. At the same time, vacancies for AI fluent strategic roles have multiplied. The labour market is being repriced rather than collapsing.

Your employees know the truth. Does your EVP? At Fathom we measure the "Credibility Gap" between your promise and their reality.

This piece draws on Bureau of Labor Statistics projections, Challenger Gray and Christmas layoff tracking, McKinsey workforce research, and a series of high profile reversals to assess what AI is actually doing to employment. It also examines what those shifts mean for employer brand, candidate trust, and the psychological contract that holds a workforce together.

The Efficiency Mirage

The first phase of the AI labour shock was almost entirely defensive. Through 2023 and 2024, large employers cut roles in customer service, content moderation, junior software engineering, and HR. Many of those cuts were framed publicly as AI substitutions. The framing was often convenient. As industry analysts have noted, when interest rates bite and revenue growth cools, one of the few levers large companies can pull quickly is headcount, and labelling those cuts as "funding our AI future" was sincere in some cases and strategic packaging in others (Computer Weekly, 2025).

A useful first step is to separate three different things that have been bundled into the "AI layoffs" headline.

The first bucket is cost-driven layoffs that AI did not cause but the AI story made easier to communicate. Post-pandemic over-hiring and higher interest rates explain much of the 2023 to 2024 contraction. The Bay Area alone added 74,700 tech jobs between 2020 and 2022, then cut 80,200 between 2023 and 2024 (Crunchbase News, 2026). Most of those reductions predate any serious enterprise AI deployment.

The second bucket is direct AI substitution attempts. Klarna, IBM's HR function, and Duolingo's contractor base are the leading examples. These are the cases where companies tried to replace humans with software and discovered the software was not yet capable.

The third bucket, visible most clearly in 2026, is AI capital expenditure consuming the headcount budget. Meta is the cleanest case. Chief executive Mark Zuckerberg told employees at an internal town hall that the roughly 8,000 planned 2026 layoffs were a direct consequence of the company's AI infrastructure spend, which Meta has guided to between USD 125 billion and USD 145 billion for the year (Tom's Hardware, 2026; Forbes, 2026). His own framing was that Meta has "two major cost centres in the company: compute infrastructure and people-oriented things". Wired reported that median total compensation at Meta fell from USD 417,400 in 2024 to USD 388,200 in 2025, and quoted one Instagram employee describing the workforce as broadly unhappy (Wired, 2026). In Meta's case, the dollars going to AI infrastructure are crowding out the dollars going to payroll, even though AI tooling has not yet replaced the underlying work.

The pure AI substitution stories that did materialise have not aged well.

Klarna offers the cleanest example. In 2023 the Swedish fintech announced its OpenAI powered assistant was doing the work of around 700 customer service agents. By spring 2025, chief executive Sebastian Siemiatkowski conceded the strategy had pushed too far. "We focused too much on efficiency and cost," he told Bloomberg. "The result was lower quality, and that's not sustainable" (Bloomberg, 2025). Klarna started hiring human agents back, this time in a flexible, distributed model that pairs them with AI rather than replacing them.

IBM ran a similar arc on its own HR function. Chief executive Arvind Krishna confirmed in 2025 that the company had used AI to absorb "a couple of hundred" HR roles, with its AskHR agent automating roughly 94% of routine tasks such as pay statement queries (Entrepreneur, 2025). The widely reported figure of 8,000 layoffs overstated the substitution picture, but the rebound was real. IBM quietly began rehiring in HR areas that required judgment, conflict handling, and accommodation work. Krishna's framing is now that AI freed up budget to invest in other roles, and that overall headcount has increased.

A professional home for employer branding. The Institute of Employer Branding Professionals is being built and you can help shape it.

Duolingo handled the same problem badly in public. In April 2025, chief executive Luis von Ahn published an "AI first" memo signalling the company would phase out contractors whose work AI could absorb. Customer backlash was rapid, and within days users were posting threats to delete the app. By August he had walked the memo back, telling the New York Times the original message "did not give enough context" (Fortune, 2025). Five months on, Duolingo had laid off no full time staff. Its contractor count rose and fell with seasonal need, while AI was being used to lift productivity rather than displace people.

The pattern that emerges is what some HR analysts have begun calling automated regret. Companies overestimate what AI can do on day one, cut the institutional knowledge that made the function work, and then quietly buy it back at a premium. HR Executive predicted in late 2025 that roughly half of AI attributed layoffs would result in some form of rehiring within 18 months (HR Executive, 2025). Churn cycles like that carry real costs, both in operational continuity and in workforce trust.

Recruitment Marketing in a Silicon Driven World

For employer brand and talent attraction leaders, the headline risk of this period has shifted from staffing levels to credibility. Candidates have watched the layoff and rehire cycle from the outside. The next time an employer markets itself as innovative, AI native, or efficiency focused, those words will land in a different context.

Two practical shifts are visible in 2026 recruitment marketing.

The first is a move away from efficiency language in candidate facing content. Where 2023 and 2024 employer brand campaigns leaned heavily on AI tooling, automation, and the promise of "doing more with less", 2026 campaigns are placing more weight on human centred language: development, mentorship, judgment, ownership, and stability. That shift is grounded in candidate sentiment. Practitioner reports and recruitment marketing observations through 2025 and into 2026 point to a consistent pattern: workers in AI exposed fields increasingly view "AI first" employers with suspicion, treating them as higher risk for sudden role redefinition.

The second is a sharper articulation of what an employee actually does in an AI augmented role. Vague promises about working with the latest tools have lost their pull, partly because the tools are now ubiquitous. The more credible employer brands are explicit about the division of labour. They describe which tasks the AI handles, which decisions remain human, what judgment is required, and how growth happens when execution is automated.

That last point matters for early career marketing. Burning Glass Institute data shows that between 2018 and 2024, the share of jobs requiring three years of experience or less fell sharply in AI exposed fields. The drop was from 43% to 28% in software development, 35% to 22% in data analysis, and 41% to 26% in consulting (Programs.com, 2025). The traditional entry level ramp has narrowed. Employers that want to attract early career talent now need to show, not just claim, how juniors will build judgment when AI is performing the work that used to teach it.

A human centric brand in a silicon driven world has become the more credible position for employers that need durable talent supply across cycles.

Visualising the Future

The data behind the AI labour story is patchy and contested. The three visualisations below summarise the most defensible patterns from public sources. They are intended as directional models, not precise forecasts.

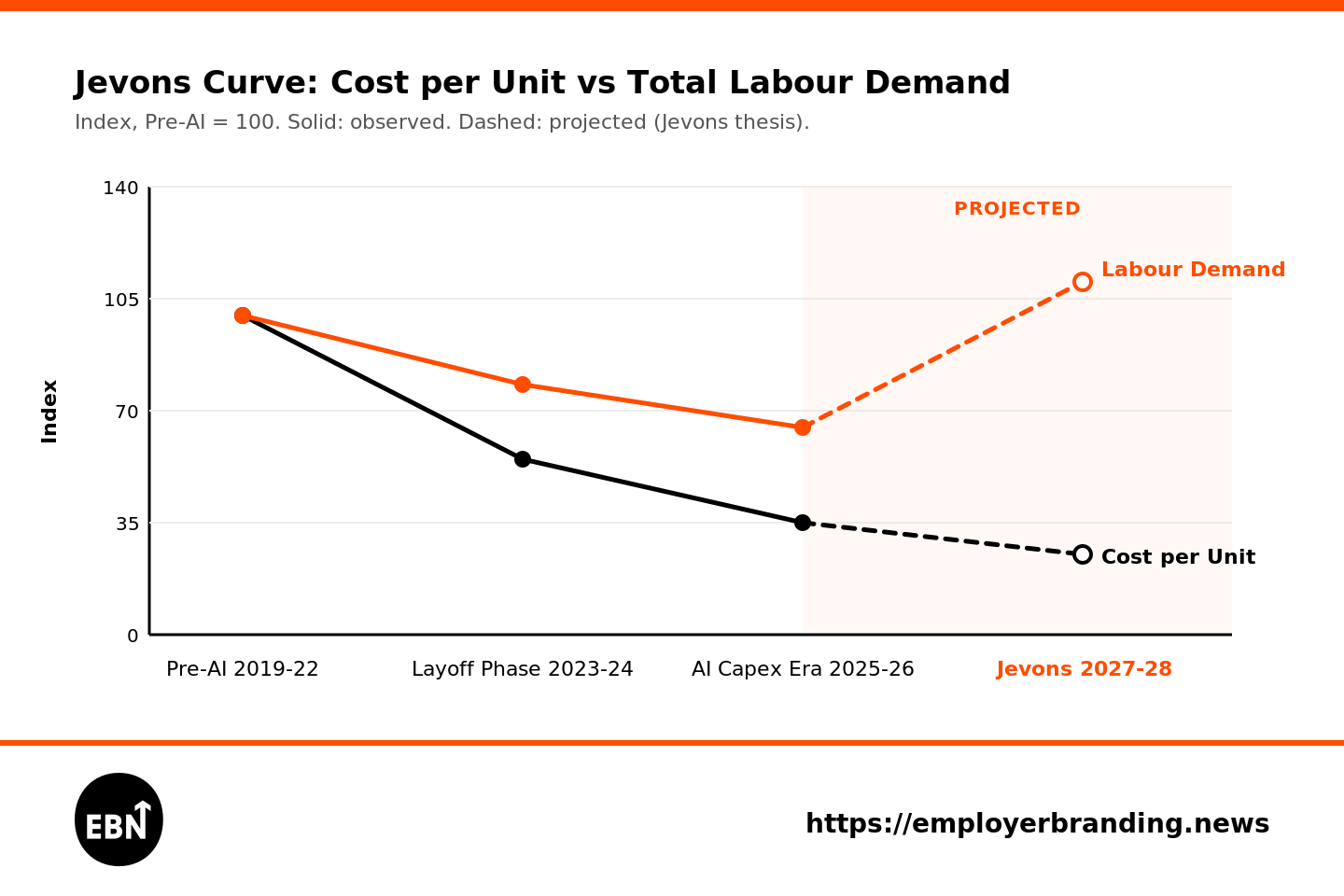

Visualisation 1: The Jevons Curve in Labour

The chart below shows the relationship between the cost per unit of cognitive output and the total demand for human labour four stages, three observed and one projected. The values are indexed to the pre-AI baseline at 100 and are directional rather than precise.

Chart explainer: the black line tracks the falling cost per unit of cognitive output as AI takes on more execution. The orange line tracks total labour demand. Through 2026 the signal points down, with continued AI-attributed cuts at scale. The dashed segment to 2027-28 is a projection grounded in the Jevons thesis: as cheaper cognition expands the universe of viable work, labour demand recovers in adjacent and previously uneconomic use cases.

| Stage | Cost per Unit of Output | Total Demand for Labour | Notes |

|---|---|---|---|

| Pre-AI (2019 to 2022) | High | Baseline plus pandemic surge | Mass hiring through the pandemic, especially in tech |

| Layoff Phase (2023 to 2024) | Falling fast | Falling in affected functions | Tech and fintech layoffs, AI cited as cause or cover |

| AI Capex Era (2025 to 2026) | Low | Still contracting in headline numbers | Aggregate AI-attributed layoffs above 48,000 in 2025, Meta and other 2026 cuts driven by AI capital expenditure |

| Jevons Realisation (2027 to 2028, projected) | Lower still | Recovering in expanded use cases | Forecast based on the Jevons thesis: cheaper cognition expands viable work into adjacent demand, supported by BLS occupational projections |

The pattern matches Jevons' original observation, but the timing is contested. As of mid-2026 the aggregate labour signal still points down rather than up. Meta's 2026 cuts, the cancellation of around 6,000 open Meta requisitions, and continued AI-attributed reductions at Microsoft and Amazon show the AI capex era is still tightening the headcount line, not loosening it. The recovery shown in the chart is therefore a projection grounded in the Jevons thesis and BLS forecasts, not a current observation. BLS projections for the 2024 to 2034 period support the directional trajectory, with software developer employment forecast to grow 15%, against 3% for all US occupations, and AI named explicitly as a demand driver (BLS, 2025).

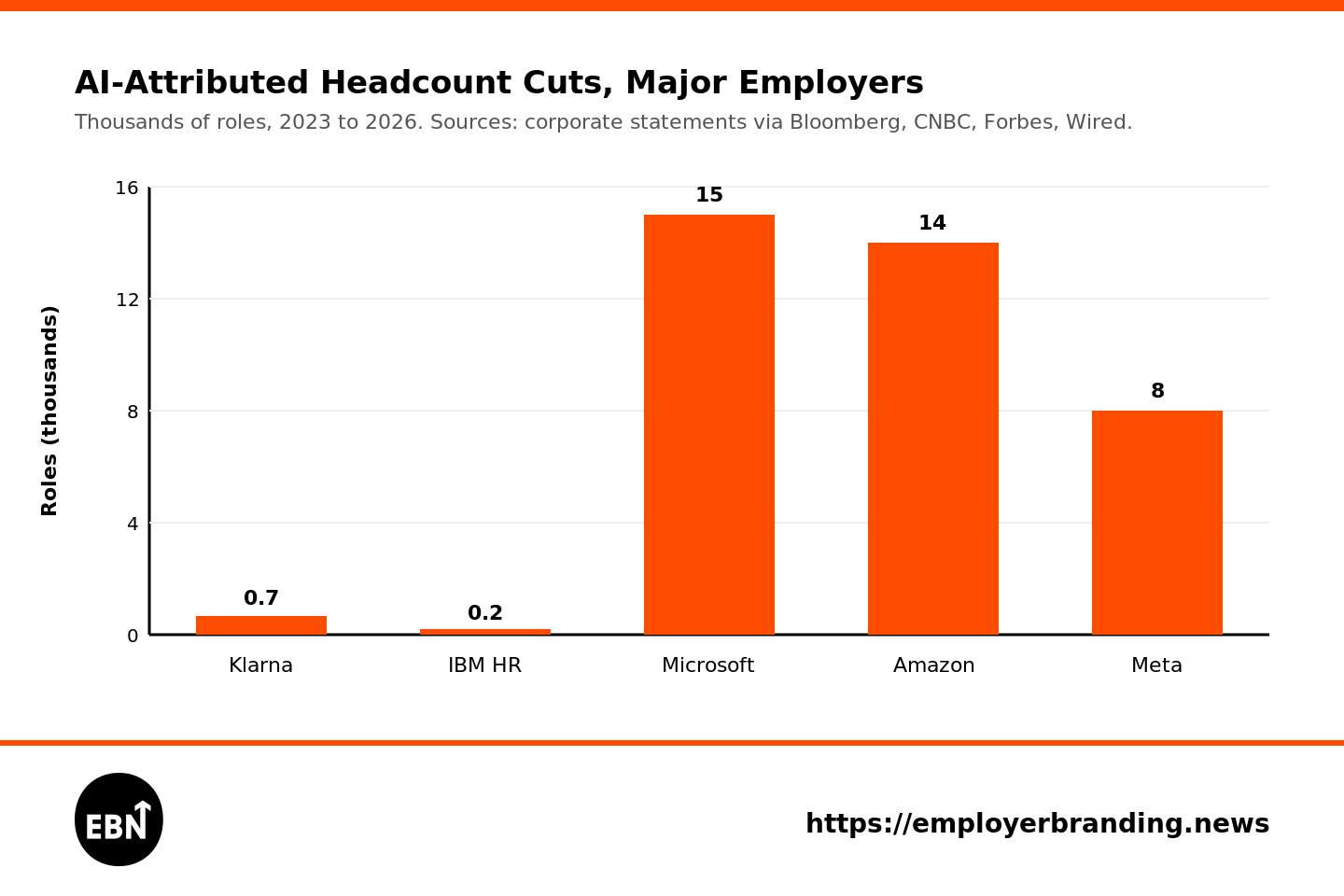

Visualisation 2: The Hiring Volatility Index

The 2024 to 2026 period has produced an unusually noisy labour signal in technology and fintech. The chart below shows AI attributed headcount cuts at major employers, in thousands of roles. It groups all three mechanisms identified earlier: direct substitution attempts (Klarna, IBM), cost-driven cuts with AI framing (Microsoft, Amazon), and AI capex-driven cuts (Meta).

Chart explainer: scale of headcount actions attributed to AI at five major employers, in thousands of roles. Klarna and IBM HR were direct substitution attempts. Microsoft and Amazon mix cost pressure with AI reallocation. Meta is the cleanest case of AI capex displacing payroll. Source numbers are cited in the table below.

The supporting detail, including subsequent hiring or reversal activity, is set out below.

| Company | AI Attributed Action | Year | Subsequent Move | Underlying Mechanism |

|---|---|---|---|---|

| Klarna | Around 700 customer service roles absorbed by AI | 2023 to 2024 | Rehiring human agents from spring 2025 | Direct substitution that failed |

| IBM | Hundreds of HR roles replaced by AskHR agent | 2024 to 2025 | Rehiring in judgment heavy HR roles, overall headcount up | Direct substitution that partially failed |

| Duolingo | "AI first" memo signalling contractor reductions | April 2025 | Memo walked back August 2025, no full time layoffs | Substitution rolled back under brand pressure |

| Salesforce | No new software engineer hires planned for 2025 | 2025 | Adding 1,000 to 2,000 salespeople for Agentforce go to market | Substitution at the margin, reallocation to commercial roles |

| Microsoft | Around 15,000 roles cut through 2025 | 2024 to 2025 | Continued hiring in AI infrastructure and research | Mixed cost and AI capex |

| Amazon | Around 14,000 corporate roles cut | 2025 | Investment redirected to AI and "biggest bets" | Cost and reallocation |

| Meta | Around 8,000 roles cut, 6,000 open roles cancelled | 2026 | More cuts not ruled out, USD 125 to 145bn AI capex | AI capex displacing payroll |

In aggregate, Challenger Gray and Christmas tracked 48,414 US layoffs in 2025 specifically attributed to AI, while a separate count put the figure at 54,694 (CNBC, 2025; Afrotech, 2025). Those numbers are real, but they sit against a US labour market that added jobs in many of the same months. The volatility itself is the story.

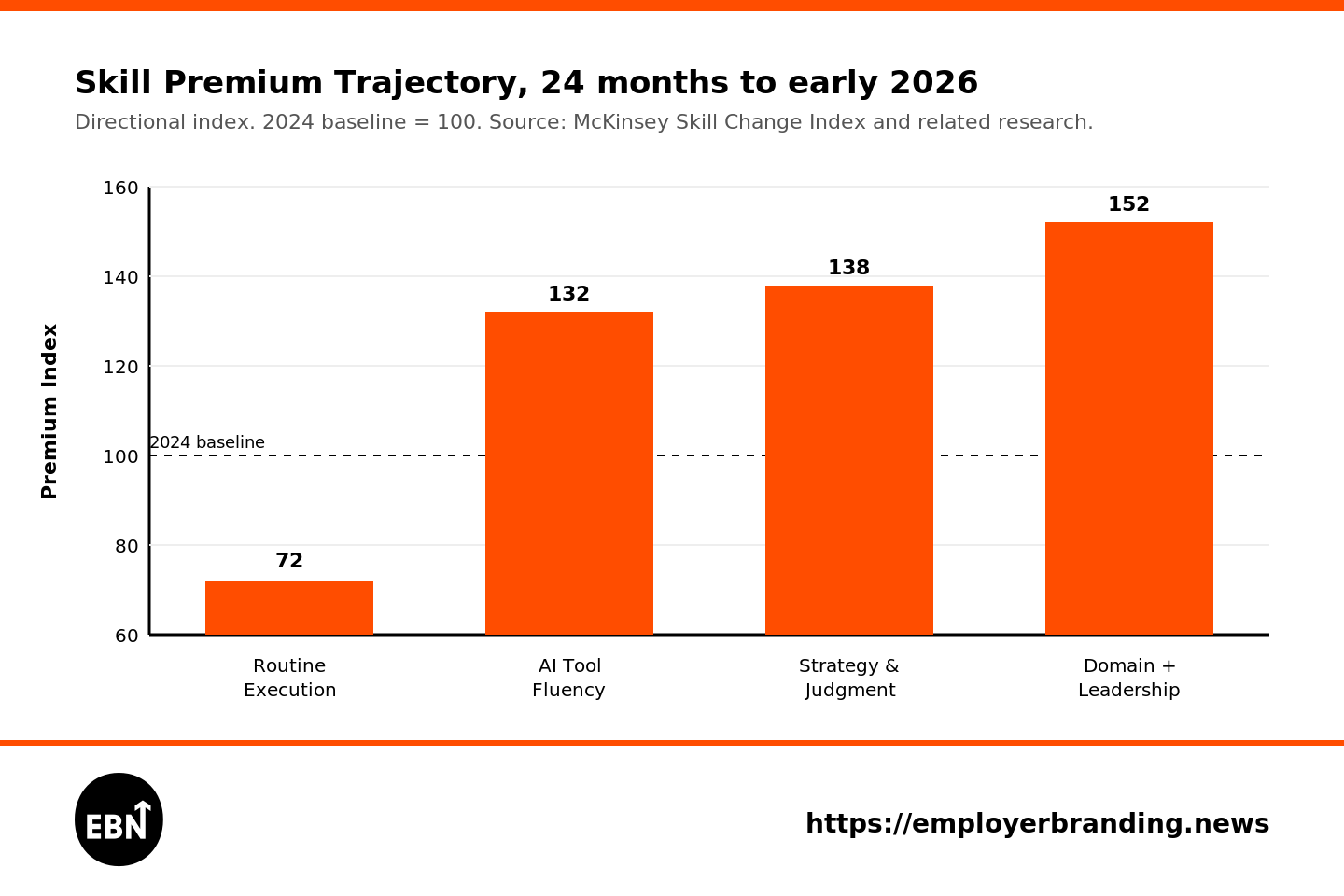

Visualisation 3: The Talent Premium Shift

McKinsey's Skill Change Index and related research point to a steady repricing of skills between execution and judgment categories over the 24 months to early 2026. The chart below is indexed to a 2024 baseline of 100 across all four categories and shows the directional movement, not absolute wage levels.

Chart explainer: directional premium index across four skill categories, baselined at 100 in 2024. Routine execution is repricing down. AI tool fluency commands a sharp short term premium that is already eroding as tools commoditise. Strategy, judgment, and senior domain plus leadership skills are the most durable beneficiaries of the AI shift, in line with McKinsey's Skill Change Index findings.

| Skill Category | Examples | Market Trajectory, 2024 to 2026 |

|---|---|---|

| Routine execution and data processing | Standard report production, first line support, basic content production | Falling premium, increasing automation exposure |

| Tool fluency with AI | Prompt design, agent orchestration, output review | Sharp short term premium, eroding as tools commoditise |

| Strategy, judgment, and orchestration | Workflow redesign, cross functional decision making, customer empathy | Rising premium, hardest to replace |

| Domain expertise plus people leadership | Senior functional roles, regulated environments, escalation handling | Strongest premium growth |

McKinsey's framing is that AI agents act as virtual coworkers, shifting the human role from executor to orchestrator. In sales, the firm reports a 30 to 50% increase in time spent on high value work such as negotiation, relationship building, and strategy, once AI takes over lead scoring and scheduling (McKinsey, 2025).

The New Leadership Mandate

The Jevons effect, if it holds, does not solve the problem people leaders are facing. It changes its shape.

The first leadership task is managing the psychological contract. Every cycle of public AI attributed cuts followed by rehiring chips away at trust, both with the people who lost their roles and with those who watched it happen. Klarna's pivot to a flexible hybrid model is partly an operational fix and partly a credibility repair. IBM's CEO has had to publicly reframe its HR cuts as part of net employment growth. Leaders who move too fast on AI substitution without a clear answer for the displaced are buying expensive lessons.

The second task is being honest about what fills the rest of the workweek. If AI takes 90% of the time out of a task, the question is what occupies the recovered hours. The credible answers fall into a small set of categories. More of the same work, serving previously uneconomic demand, which is the Jevons effect at the individual level. Expanded scope into adjacent decisions and stakeholder management. Deeper specialisation. Genuine recovery time. The least credible answer, and the one most likely to be quietly true, is that people will work the same hours producing more output until expectations recalibrate. Leaders who fail to make a deliberate choice between these models risk burnout and attrition that will not appear in any AI productivity report.

The third task is rebuilding the entry level ramp. With early career roles in AI exposed fields shrinking, the apprenticeship logic that produced senior talent in the previous era is breaking down. Some employers are responding with structured AI augmented graduate programmes that deliberately slow down execution so juniors can practise judgment. Others are quietly outsourcing the problem and assuming senior hires will keep arriving. The labour market will reward the first group within five to ten years.

Employer branding now has a measurement standard. The Talent Gravity Standard is a six-driver framework for quantifying employer attractiveness and the gap between brand promise and employee experience.

The fourth task is honest forecasting. Mass hiring for growth, in the form seen in tech between 2020 and 2022 when the Bay Area alone added 74,700 tech jobs before cutting 80,200 in 2023 and 2024 (Crunchbase News, 2026), is unlikely to return in the same shape. What replaces it is a leaner baseline with periodic surges in narrower, higher value roles. Workforce planning for that pattern looks very different from headcount planning for the previous cycle.

What Employer Brand Leaders Should Plan For Now

The analytical picture is one thing. The practitioner question is what to do about it on Monday morning. For employer brand, talent attraction, and people communications leaders, five planning priorities sit higher than they did 18 months ago.

1. Audit AI-first language across owned channels. Careers sites, recruitment marketing campaigns, LinkedIn life pages, and Glassdoor responses written between 2023 and 2025 often lean hard on efficiency, automation, and "AI-native" positioning. The Klarna and Duolingo reversals have made that language a liability. Employer brand teams should run a content audit, identify pages that overcommit to AI-first messaging, and rewrite them around the concrete division of labour between people and tools. Treat this as a credibility hedge against the next reversal cycle, with the cosmetic rebrand value as a bonus.

2. Rebuild the EVP around judgment, mentorship, and stability. Where 2023 EVPs leaned on tooling and pace, 2026 EVPs are landing better when they describe how the employer develops judgment, supports growth from junior to senior, and protects employees through volatility. This shift is most visible in finance, consulting, and law, where the Jevons logic predicts expansion in human-judgment roles. EB leaders should also reconsider how they describe career progression in functions where the entry level ramp has narrowed. Vague growth promises will not survive the first time a candidate's friend gets laid off in the same role.

3. Develop a credible "recovered time" story. Every AI-augmented role has a 90% question. If the AI handles most of the execution, what fills the rest of the workday? The answer must be specific by function. Sales teams might point to McKinsey's 30 to 50% increase in time spent on negotiation and relationship building. Product teams might point to expanded experimentation cycles. Customer service teams might point to time spent on complex escalations and customer relationship work. Vague answers signal that leadership has not actually thought it through, and candidates can tell.

4. Plan for the rehire and boomerang narrative. If HR Executive's prediction holds and roughly half of AI-attributed layoffs end in some form of rehiring, employer brand teams should plan for this in advance. That means alumni network strategy, a clean rehire process, and a public position on AI-led decisions that does not require reversal. It also means preparing internal communications for the scenario where former colleagues return. The IBM and Klarna stories suggest this scenario is now common enough to plan for, not exceptional enough to improvise around.

5. Treat layoff communications as an EB issue, not just an HR ops issue. The Meta example shows what happens when an AI-driven layoff is framed bluntly to employees as a budget line item. Wired's reporting on Meta's "bad vibes" is now part of the company's permanent employer brand context, alongside any positive recruitment marketing. EB leaders should be at the table when AI-related restructuring is being planned, with explicit authority to shape internal and external messaging. Brand recovery from a poorly handled layoff cycle takes years, not quarters.

A practical lens for prioritising these five items: which of them would a candidate, a journalist, or a current employee most easily exploit to embarrass the company in the next 12 months. That tends to point at the right place to spend the next quarter's effort.

Conclusion: A Balanced View of Labour Volatility

The most honest reading of the 2024 to 2026 labour data is that AI is restructuring work, with effects that are uneven across roles, sectors, and career stages.

The Jevons paradox helps explain why total labour demand has not collapsed. As the cost of cognitive work falls, the universe of work expands, and human attention moves up the value chain to judgment, decision making, and orchestration. The Klarna, IBM, and Duolingo reversals show that even employers with strong technical capability misjudged how much human judgment was embedded in the roles they tried to automate. The McKinsey and BLS data show real growth in AI adjacent roles even as parts of the entry level ramp narrow.

Where the optimistic Jevons reading is incomplete is in distribution. A world with more lawyers but fewer law firm associates is not obviously a victory for the workers most at risk, and a similar pattern is visible in software, consulting, and analysis. Aggregate demand for labour can rise while specific groups, especially early career workers in AI exposed fields, face a harder market than their predecessors did.

For people leaders, the practical implication is to plan for volatility rather than equilibrium. The cycle of efficiency optimism followed by automated regret will repeat, probably more than once. The employers that come out of it with intact brands, trusted relationships with their workforce, and a defensible talent pipeline will be the ones that resist the impulse to treat AI as a headcount lever, and instead use it as a redesign tool.

That is a less dramatic story than either "AI ends work" or "AI creates jobs for everyone". It is also closer to what the evidence currently shows.

References

- Apollo Global Management / Fortune. Torsten Slok on the "Jevons employment effect". Fortune, 2026. https://fortune.com/2026/04/28/will-ai-kill-jobs-why-not-jevons-paradox-torsten-slok/

- Bloomberg. Klarna Turns From AI to Real Person Customer Service. 8 May 2025. https://www.bloomberg.com/news/articles/2025-05-08/klarna-turns-from-ai-to-real-person-customer-service

- Bureau of Labor Statistics. AI impacts in BLS employment projections. The Economics Daily, 2025. https://www.bls.gov/opub/ted/2025/ai-impacts-in-bls-employment-projections.htm

- Challenger, Gray and Christmas, via CNBC. "AI was behind over 50,000 layoffs in 2025." 21 December 2025. https://www.cnbc.com/2025/12/21/ai-job-cuts-amazon-microsoft-and-more-cite-ai-for-2025-layoffs.html

- Computer Weekly. Tech sector layoffs mount amid AI investment frenzy. 2025. https://www.computerweekly.com/news/366606035/Tech-sector-layoffs-mount-amid-AI-investment-frenzy

- Crunchbase News. Tech Layoffs: US Companies With Job Cuts In 2024, 2025 and 2026. https://news.crunchbase.com/startups/tech-layoffs/

- Entrepreneur. IBM CEO: AI replaced hundreds of HR staff. 2025. https://www.entrepreneur.com/business-news/ibm-ceo-ai-replaced-hundreds-of-human-resources-staff/491341

- Fortune. Duolingo CEO admits his controversial AI memo "did not give enough context". 18 August 2025. https://fortune.com/2025/08/18/duolingo-ceo-admits-controversial-ai-memo-did-not-give-enough-context-insists-company-never-laid-off-full-time-employees/

- HR Executive. The AI layoff trap: Why half will be quietly rehired. 2025. https://hrexecutive.com/the-ai-layoff-trap-why-half-will-be-quietly-rehired/

- McKinsey and Company. Redesigning technology workforce for the agentic AI era. 2025. https://www.mckinsey.com/capabilities/mckinsey-technology/our-insights/designing-an-end-to-end-technology-workforce-for-the-ai-first-era

- McKinsey and Company. Rethink management and talent for agentic AI. 2025. https://www.mckinsey.com/capabilities/people-and-organizational-performance/our-insights/the-organization-blog/rethink-management-and-talent-for-agentic-ai

- NPR Planet Money. Why the AI world is suddenly obsessed with Jevons paradox. 4 February 2025. https://www.npr.org/sections/planet-money/2025/02/04/g-s1-46018/ai-deepseek-economics-jevons-paradox

- Programs.com. Burning Glass Institute data on entry level role share in AI exposed fields. 2025. https://programs.com/resources/ai-layoffs/

- Salesforce Ben. Salesforce Will Hire No More Software Engineers in 2025, Says Marc Benioff. 2025. https://www.salesforceben.com/salesforce-will-hire-no-more-software-engineers-in-2025-says-marc-benioff/

- Afrotech. AI led to 48,000 US layoffs in 2025 (Challenger Gray and Christmas data). 2025. https://afrotech.com/in-2025-alone-ai-has-led-to-48000-layoffs-in-the-us

- Forbes. Mark Zuckerberg says AI costs contributed to layoffs of 8,000 staffers, report says. 30 April 2026. https://www.forbes.com/sites/antoniopequenoiv/2026/04/30/mark-zuckerberg-says-ai-costs-contributed-to-layoffs-of-8000-staffers-report-says/

- Wired. Inside Meta's morale crash and AI driven layoffs. April 2026. https://www.wired.com/story/meta-layoffs-bad-vibes-mark-zuckerberg-ai/

- Tom's Hardware. Mark Zuckerberg says Meta is cutting 8,000 jobs to pay for AI infrastructure. May 2026. https://www.tomshardware.com/tech-industry/big-tech/mark-zuckerberg-says-meta-is-cutting-8000-jobs-to-pay-for-ai-infrastructure

- Fortune. Mark Zuckerberg has cut 25,000 jobs at Meta since 2022. 27 March 2026. https://fortune.com/2026/03/27/mark-zuckerberg-meta-layoffs-metaverse-reality-labs-year-of-efficiency-tech-ai/

Note on methodology: Layoff and rehire figures are drawn from corporate statements, Bloomberg, CNBC, Fortune, and Challenger Gray and Christmas tracking. Where company reported and third party figures diverged, the lower verified figure has been used. The article distinguishes between AI as a cited cause of layoffs and AI as a verified cause of substitution. As multiple sources note, much of the 2023 to 2024 tech contraction is more accurately attributed to post pandemic over hiring and interest rate pressure, with AI playing a secondary role in many cases.